News

Nvidia Tops WSJ’s Best Companies for the Future Ranking

The Wall Street Journal’s inaugural Best Companies for the Future ranking places Nvidia at No. 1, with Alphabet, Microsoft, Meta Platforms, and Cisco completing a top five driven by AI readiness.

The Wall Street Journal’s inaugural Best Companies for the Future ranking placed Nvidia at No. 1, putting a chip designer that closed fiscal 2026 with $215.9 billion in revenue at the top of what may become the decade’s most consequential corporate scorecard. The full top five, per the Journal, is Nvidia, Alphabet, Microsoft, Meta Platforms, and Cisco Systems, a group it credits with strong scores in innovation, financial strength, and AI readiness. The Journal defines that last metric as how prepared a company is for an AI-centric future, measured across its operations, its investments, and its people.

Publishing the list also formalizes AI readiness as a scoreable benchmark alongside financial strength and innovation. Institutional investors covering the S&P 500 now have a named framework to run against every company that didn’t place, and the inaugural edition creates a baseline each future edition will measure movement against.

The Inaugural Top Five

Nvidia placed first or second in five of the ranking’s six main scoring components, the Journal reports, a spread no other company matched. Three of those six components are publicly named: innovation, financial strength, and AI readiness. The methodology doesn’t specify the other three.

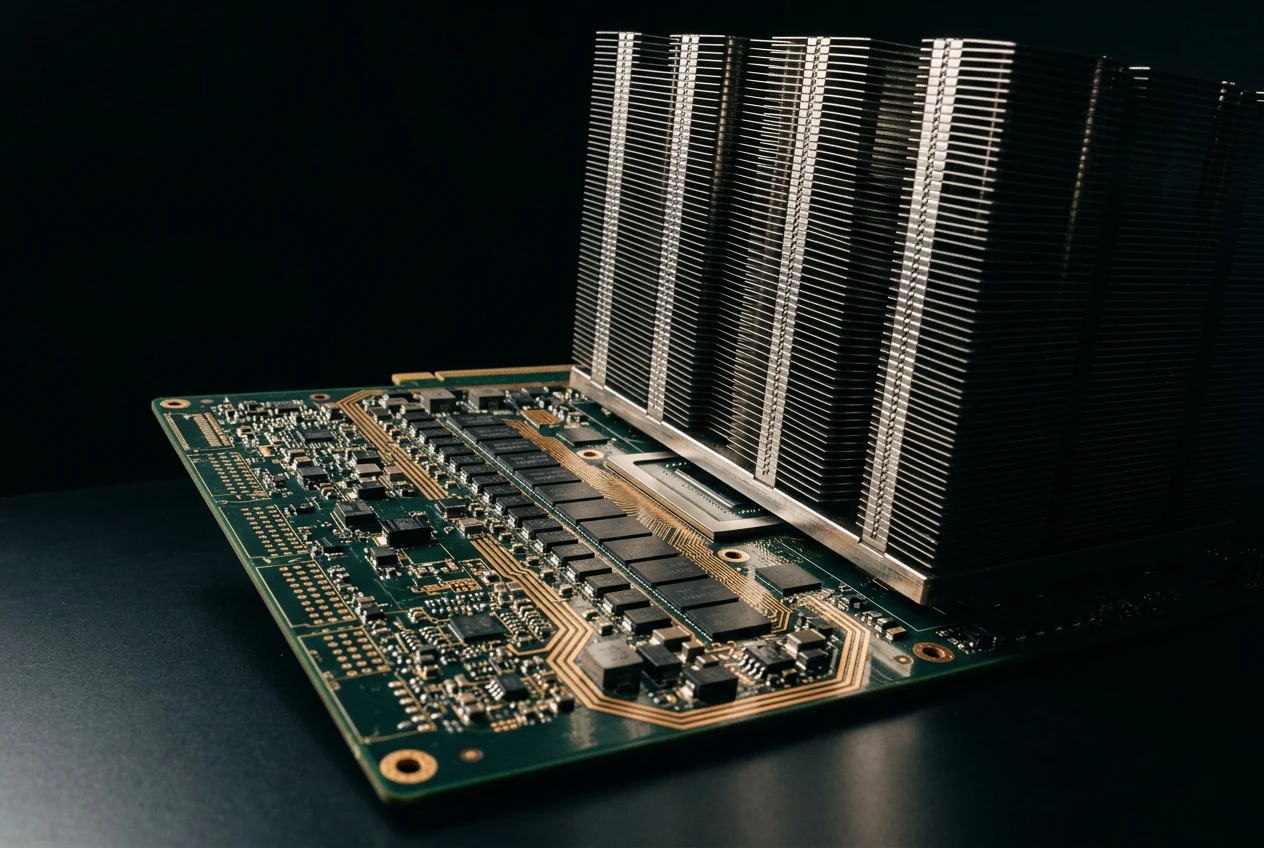

- $193.7 billion – Nvidia Data Center segment revenue in fiscal 2026, roughly 90% of total annual revenue

- 65% – year-over-year revenue growth for Nvidia in fiscal 2026

- 5 of 6 – WSJ ranking components where Nvidia placed first or second

- ~$5.2 trillion – Nvidia market capitalization, the highest of any publicly traded company globally

Four companies share the top five with Nvidia, each occupying a distinct lane in the AI economy. Alphabet holds Google Cloud and designs its own AI accelerator chips, Tensor Processing Units (TPUs), which it deployed internally for more than a decade and now offers externally; Google Cloud revenue grew 34% in its most recent quarter. Microsoft operates the Azure cloud and holds a 27% stake in OpenAI, with exclusive intellectual property rights to its large language models through 2032; Azure grew 40% last quarter, driven by AI services. Meta Platforms deploys AI across its advertising and recommendation systems and publishes its Llama open-weight model family as a freely accessible alternative to proprietary models. Cisco Systems provides the network hardware and security systems that AI workloads pass through inside and between data centers.

| Company | Core AI Role | 2026 Capex Guidance |

|---|---|---|

| Nvidia | GPU supply chain for AI training and inference | Fabless model; receives hyperscaler capex |

| Alphabet | Google Cloud, TPU chips, Gemini AI models | $175 billion to $185 billion |

| Microsoft | Azure AI, Copilot platform, OpenAI stake | ~$190 billion |

| Meta Platforms | Ad AI targeting, Llama open-weight models | $115 billion to $135 billion |

| Cisco Systems | AI networking and security infrastructure | Network-layer supplier |

How the Six Components Score

Three Named Pillars

The Journal publicly identifies three of its six ranking components: innovation, financial strength, and AI readiness. The AI readiness definition is the most specific, covering how deeply AI is embedded in a company’s operations, how much capital it has directed toward AI infrastructure and talent, and how AI-oriented its workforce is. That third element stretches the metric beyond capital spending. A company can direct billions into AI infrastructure and still score poorly if its employees lack the skills to use it productively.

The structure mirrors what Cisco’s annual AI Readiness Index has tracked across enterprise organizations since 2023. Cisco’s third annual AI Readiness Index, published in October 2025, covered 8,000 senior IT and business leaders across 30 markets and 26 industries using six readiness pillars: strategy, infrastructure, data, talent, security, and culture. The conceptual overlap with the Journal’s methodology, while the specific companies ranked differ, points to broader industry convergence on what rigorous AI readiness measurement tracks at the corporate level.

Nvidia’s Five-of-Six Record

Against those components, the arithmetic behind Nvidia’s scores follows from its financial position. Its fiscal 2026 annual results show $215.9 billion in total revenue, up 65%, with the Data Center segment growing 68% to $193.7 billion. That segment accounts for roughly 90% of total revenue, all tied to the graphics processing units (GPUs) that train and run AI models. Nvidia’s Blackwell GPU architecture, ramped during fiscal 2026, is the compute platform every major model lab and hyperscaler is currently building on. The company also returned $41.1 billion to shareholders in fiscal 2026 through $40.1 billion in buybacks and $974 million in dividends.

The IMD Center for Future Readiness, which publishes a parallel corporate preparedness exercise independently of the Journal, gave Nvidia a perfect 100.0 score in its Technology Future Readiness Indicator for 2026, with Microsoft at 93.3 and Alphabet at 91.7. The IMD’s methodology and the Journal’s are distinct, but the directional alignment between two independent frameworks reinforces the outcome. The IMD described the current period as one where “infrastructure dominance” has replaced product cycles as the defining factor in tech sector competition, a shift Nvidia’s revenue composition reflects most completely.

The one component where Nvidia placed lower than first or second remains unspecified in the Journal’s public methodology. That gap limits how precisely companies outside the top five can benchmark themselves against the leaders.

Why Cisco Made the List

Among the five, Cisco occupies a structurally different position. The company designs no AI chips and trains no large language models. Its ranking comes from the switches, routers, and security systems that AI workloads pass through inside and between data centers.

Infrastructure spending is cool again.

Cisco CEO Chuck Robbins said that on Yahoo Finance’s Opening Bid, citing the rise of AI data center construction as the driver of enterprise network spending. As enterprises move from AI pilot to AI production, the network layer carrying those workloads becomes the next scaling constraint. Cisco’s own research found that only 15% of companies have networks fully ready for AI, while 71% of what it calls Pacesetters, organizations already achieving measurable AI value, have fully flexible and instantly scalable networks deployed.

The same study found that 84% of Pacesetters have end-to-end encryption with continuous monitoring, versus 30% of all organizations. Security infrastructure and centralized data access are the two gaps the study cites most consistently as blockers to AI deployment at production scale, and Cisco’s portfolio addresses both. A separate finding: 83% of organizations surveyed plan to deploy AI agents within a year, but few have built the secure infrastructure to operate them at scale.

Cisco has described the current period as a networking supercycle, driven by AI’s latency and bandwidth requirements exceeding what legacy enterprise infrastructure was designed to handle. Its switching platforms and AI-ready data center architectures are positioned as the upgrade path for enterprises moving from isolated pilots to organization-wide deployment. The company also deploys AI in its own network management and security products, giving it a position on the operational dimension of the AI readiness metric it sells to customers.

The Capital That Reinforces the Scores

The four hyperscalers most closely associated with the WSJ top five, Alphabet, Microsoft, and Meta Platforms, along with Amazon, plan to collectively allocate $725 billion in capital expenditures for 2026, up from the $410 billion they deployed the prior year. The individual figures: Alphabet is targeting $175 billion to $185 billion, Microsoft is tracking toward $190 billion, and Meta Platforms is guiding $115 billion to $135 billion. A substantial portion of that spend flows through Nvidia’s GPU supply chain and software stack.

Nvidia’s first-quarter fiscal 2027 earnings, reported May 20, 2026, put quarterly revenue at $81.6 billion, up 85% year-over-year. Data Center alone was $75.2 billion, up 92%. Jensen Huang, Nvidia’s founder and chief executive, described the pace of infrastructure build-out in that earnings report as the largest infrastructure expansion in human history, accelerating at extraordinary speed.

The reinforcing dynamic is structural. Nvidia’s CUDA software layer, on which major AI labs and enterprises have built their model development pipelines, creates switching costs that keep Data Center revenue recurring even as alternative GPU suppliers expand. The hyperscalers driving Nvidia’s revenue are also the companies whose capex commitments make that revenue broadly predictable a quarter in advance. Companies that started building AI infrastructure in 2025 or later face both higher hardware costs and a more entrenched competitive landscape.

A New Benchmark for Every Boardroom

Cisco’s AI Readiness Index found that 13% of organizations qualify as full Pacesetters, those consistently able to move AI from pilot to production at scale. Those companies are four times more likely to advance AI projects into production and 50% more likely to report measurable value from deployments. The other 87% have faced that gap in internal surveys. The WSJ ranking assigns it a public label at the peer-company level for the first time.

Healthcare, manufacturing, and financial services are the sectors where the gap is widest. Each employs large workforces where building AI orientation quickly is difficult, and each faces regulatory constraints that slow AI deployment from pilot to production. Those are precisely the barriers Cisco’s survey identified most frequently as blockers.

Fund managers holding companies outside the top five now have a named benchmark to invoke in earnings calls. The three publicly named components, innovation, financial strength, and AI readiness, map onto existing analyst frameworks closely enough that sector-level comparisons will follow. Companies in every major industry face pressure to score themselves against a framework that now carries the Journal’s editorial weight.

- Investor scrutiny: The inaugural edition gives institutional investors a specific, publishable benchmark to reference against portfolio companies across every sector, with movement trackable across future editions.

- Board-level accountability: The six-component methodology creates board-level pressure to address AI readiness, financial strength, and innovation in formal disclosures, particularly for companies in regulated industries.

- Talent strategy: The Journal’s AI readiness definition explicitly includes workforce AI orientation, placing the metric on every chief people officer’s agenda alongside conventional succession and retention tracking.

The first edition of this ranking tells every S&P 500 company not on it exactly where it stands on the metric the next edition will measure.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. The companies discussed are publicly traded, and their financial results and ranking positions are subject to change. Readers should consult a qualified financial professional before making any investment decisions. Figures are accurate as of publication.

Redmi Battery Monsters Win the Week as Samsung Trims S27 Cameras

Moto G Max India Bet Puts 7000mAh Battery Ahead of Specs

Take-Two CEO Pushes Netflix Subs for GTA 6 Extended Look

Google Bets Tensor G6 Efficiency Fixes Pixel’s Old Flaws

Grok Image 2.0 Adds Pro Edits While Scandals Linger

Caviar Leather iPhone 18 Pro Editions Kill Wireless Charging for Status

Quordle Monday Delivers Gavel Crush Speed Ethos Cleanly

Goldmund Telos 9800 Mono Amp Costs More Than Most Ferraris

Gemini Plan Dropped the Race and Made Running Stick

Cloudflare Kitesurf Cracks Chromium Moat for AI Agents

SpaceX Preps Starship Flight 13 to Fix Its Booster Failure

PS5 Adds a Weekly Wrap-Up Widget While Recently Played Stays Broken

Tears of the Kingdom Fans Trap Ganondorf in a Never-Ending Hamster Wheel

ZA/UM Lays Off 32 Staff as Zero Parades Wins Reviews, Not Players

EA’s New In-Game Ad Platform Skips the Games That Need It Most

Wall Street’s SpaceX and Merger Fee Boom Comes With a Catch

Pentagon Suspends CMMC Phase 2, Relieving Small Firms, Straining Assessors

Colorado’s New Law Makes Automakers Own Dead EV Batteries

Mortgage Rates Climb to 6.55%, the Highest Level in Nearly a Year

Perseid Meteor Shower Begins This Week Under a Rare Earthshine Moon

-

TECHNOLOGY3 years ago

TECHNOLOGY3 years agoHow to Adjust a Bulova Watch Band – An Easy Guide

-

News3 years ago

News3 years agoFred Pentland: Athletic Bilbao’s English mentor who changed the essence of Spanish football

-

FINANCE3 years ago

FINANCE3 years agoTax Planning for Every Season: Guide to Maximizing Your Tax Benefits

-

Education3 years ago

Education3 years agoAfrican Ministers New Education Plan

-

BUSINESS3 years ago

BUSINESS3 years agoWhat is Entrepreneurial Operating System? A Comprehensive Guide to EOS

-

Education3 years ago

Education3 years agoInnovate Your Learning Journey with Technology and Enhance Education

-

BUSINESS3 years ago

BUSINESS3 years agoTop 9 Most Expensive American Cities to Rent an Apartment

-

News3 years ago

News3 years agoRussians formally out of World Athletics Championships