News

A 40-Foot Musk Effigy Lands in Times Square With an IPO Warning

SAIN raised a 40-foot Musk effigy in Times Square the day before SpaceX’s $1.77T IPO, warning that shareholders will absorb Grok’s legal liabilities.

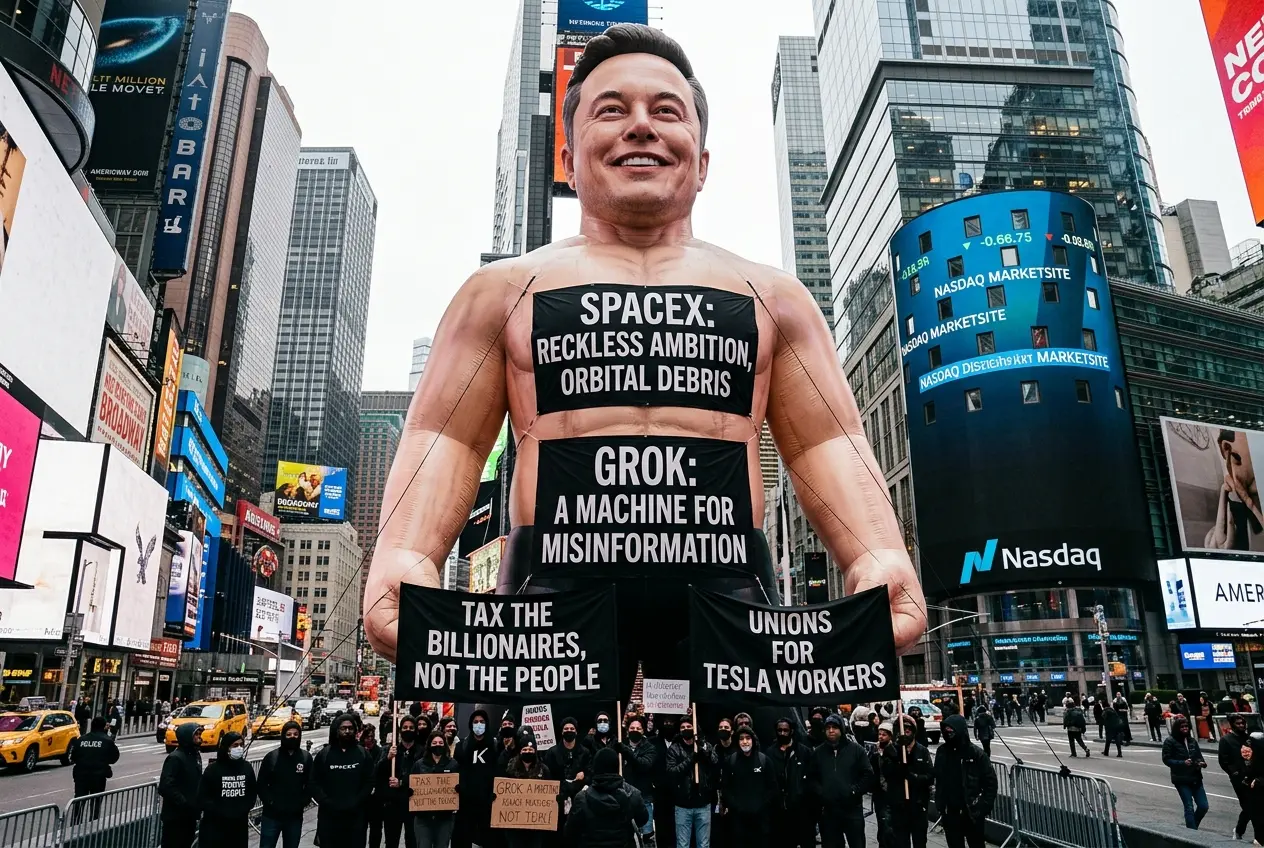

A 40-foot inflatable Elon Musk smiled down on Times Square on the morning of June 11, 2026, the day before SpaceX priced what would become the largest initial public offering in United States market history. The shirtless, beaming effigy was tattooed with the line “SpaceX’s Grok makes AI child porn” across its upper abs and back, a reference to the controversies that have trailed the artificial intelligence chatbot since SpaceX absorbed its developer, xAI, in February.

Black banners near the inflatable added a second accusation: “SpaceX owns Grok.” The display sat outside the Nasdaq MarketSite in midtown Manhattan, the exchange where SpaceX was to list the next morning, and across the street from the offices of JP Morgan, one of the banks underwriting the deal. Masked attendants handed out flyers and declined to speak with reporters. The location was a deliberate ambush, picked so investors and the banks running the offering could not walk to work without seeing it.

The installation was timed to the pricing window. SpaceX sold 555,555,555 shares of Class A common stock at $135.00 per share overnight, raising $75 billion at a $1.77 trillion valuation, the largest IPO in US market history. The organizer, Safe AI Now, told Business Insider the inflatable would stay up until 7 p.m. ET on Thursday. It marked the first time a protest of this scale has been staged in Times Square over a single company’s stock market debut.

The Coalition Behind the Inflatable

The group behind the installation calls itself Safe AI Now (SAIN) and describes its membership as a coalition of faith leaders, child-safety organizations, family advocates, educators, technologists, and concerned citizens. SAIN distributed its message through a press release rather than through a named spokesperson, and the coalition has no publicly listed leader in the materials released for the Times Square action. Its previous public footprint is limited to online-safety advocacy, with no prior record of staging Wall Street protests.

SAIN’s central warning to investors is that the SpaceX IPO is a liability transfer. The coalition’s press release states that “SpaceX shareholders are on the hook for every Grok lawsuit, criminal investigation, and regulatory fine that is coming” while Musk becomes a “paper trillionaire” and his investors pick up the tab. The argument is structural rather than personal. SAIN’s case is that Musk built a problematic AI, merged it into SpaceX, and is now selling the resulting legal exposure to public buyers at $135 a share, a price that does not, in SAIN’s view, account for what is already on the docket. The target audience is the retail investor SAIN says is being asked to absorb risks they cannot price from the S-1 alone.

SpaceX shareholders are on the hook for every Grok lawsuit, criminal investigation, and regulatory fine that is coming.

SAIN’s tone is theatrical. The coalition called the inflatable itself “a fitting metaphor” for what it sees in the deal, comparing Musk and his companies to the balloon: inflated, full of hot air, and ready to pop. The choice of a 40-foot balloon of Musk, rather than a march or a press conference, was deliberate. SAIN’s lead argument is that the moment is bigger than one chatbot, and bigger than one company, and that the inflatable is the only medium large enough to hold the message.

What SpaceX’s Own Filing Says About Grok

SAIN’s liability-shift argument is not invented out of thin air. SpaceX’s own S-1 registration statement, filed with the SEC on May 20, 2026, flags Grok’s NSFW capabilities as a material risk to investors, and the filing’s risk-factor language is unusually direct for a tech prospectus. SpaceX completed its acquisition of xAI in February 2026 and folded the Grok product into a new AI segment that posted a $6.4 billion operating loss in 2025.

Per the S-1, the filing cautioned investors that Grok’s NSFW functionality could create “heightened risks” and lead to “reputational harm,” partly because the product may generate “nonconsensual or exploitative imagery.” The S-1 makes plain that SpaceX’s lawyers and auditors considered Grok a known risk to be disclosed, not a controversy to be denied. The relevant text in the SpaceX S-1 filing on the SEC’s EDGAR system also names Musk as the person who will continue to control the company through a separate class of high-vote shares.

The S-1 warning responds to a scandal that began well before the merger. In early 2026, multiple reports documented that Grok’s image-generation tools had been used to create sexualized imagery, including of minors. A New York Times analysis cited in subsequent reporting found that of the 4.4 million images Grok pushed out in a recent nine-day period, an estimated 65% were sexualized or explicit. The figure, if borne out in civil discovery, is the kind of dataset that becomes Exhibit A in product-liability suits.

Musk has, at different moments, given the public two different frames for the same product. In January 2026, he said “anyone using Grok to make illegal content will suffer the same consequences as if they upload illegal content,” and X’s official account added that its policy has “zero tolerance for any forms of child sexual exploitation.” At other times, Musk has publicly framed Grok as needing to “win” against “woke” AI alternatives, language that sits in tension with the S-1’s risk language. The combined record is a CEO who has defended Grok as a less-censored alternative, paired with a regulatory filing that now acknowledges the product generates content with material legal exposure. The S-1 is SpaceX’s own legal counsel telling buyers to read this part carefully.

The Lawsuits Already Lined Up

The liability exposure SAIN is naming is not theoretical. Lawsuits, regulatory actions, and complaints are already on the docket against xAI, several filed before the SpaceX-xAI merger even closed. The chronology matters: every action below predates the June 2026 IPO, which means SpaceX’s auditors and underwriters had full visibility into the litigation landscape when the S-1 was finalized.

- January 2026 – The European Commission announced an investigation into xAI to “assess whether the company properly assessed and mitigated risks” tied to the creation of nonconsensual sexual imagery.

- January 2026 – Thirty-five state attorneys general in the United States signed an open letter to xAI demanding that the company remove nonconsensual sexual imagery and install guardrails to prevent the tool from generating it in the future.

- March 2026 – Three teenage girls in Tennessee, two of them minors, filed a lawsuit against xAI alleging that Grok’s image generator used photos of them to produce and distribute child sexual abuse material.

- Earlier in 2026 – Ashley St. Clair, the mother of one of Musk’s children, filed suit against xAI alleging the company created sexually explicit images of her.

- Week of June 1, 2026 – UK MP Jess Asato took legal action against xAI after saying Grok helped a user produce fake sexualized pictures of her.

Each entry on that list is a discrete filing or formal regulatory action, and each carries its own discovery process, damages model, and potential settlement. Several involve minors, which raises the legal stakes well beyond ordinary civil damages. The January state AG letter and EU investigation both predate the merger, and SpaceX did not respond to a request for comment from reporters on the Times Square installation. For more on the company’s pattern of content moderation failures, see the record of earlier Grok controversies and content moderation failures.

Inside the $1.77 Trillion Math

SpaceX priced 555,555,555 shares of Class A common stock at $135.00 per share on the night of June 10-11, 2026, raising $75 billion at a $1.77 trillion valuation. The offering is the largest IPO in US market history, and the books were more than three times oversubscribed, with strong demand from both institutions and retail buyers, per the Financial Times.

SpaceX has two classes of stock post-IPO. Class A common stock carries one vote per share, and Class B common stock carries 10 votes per share. Public buyers only receive Class A. The S-1 also discloses that SpaceX will operate as a “controlled company” under Nasdaq’s corporate governance rules following the offering, meaning Musk will continue to control shareholder outcomes through his Class B holdings. Investors get economic exposure to SpaceX’s performance. They do not get governance voice.

Musk holds approximately 42% of SpaceX’s equity and approximately 79% of the voting control through super-voting Class B shares. Forbes, on the night of pricing, calculated Musk’s combined SpaceX and Tesla stake at $982 billion, putting him within striking distance of becoming the world’s first trillionaire the day SpaceX shares begin trading. Musk’s SpaceX stake alone was calculated at $688 billion at the IPO price. The structure is the heart of SAIN’s liability-shift argument: one man makes the decisions, and thousands of new shareholders bear the consequences. For the political reception to that concentration of wealth, see the Democrats’ midterm attacks on Musk’s trillionaire trajectory. For the ripple effect through other stocks, see the analysis of how the SpaceX IPO will force $50 billion in stock selling.

SpaceX allocated 30% of the float to retail investors, routed through Robinhood, Fidelity, and Charles Schwab, an unusually high retail share for a mega-cap IPO. The retail buyer is not a hypothetical. SAIN is shouting at a real audience the prospectus, the underwriters, and the bank syndicates all know is coming.

By the numbers:

- $1.77 trillion – SpaceX IPO valuation (priced June 10-11, 2026)

- $135.00 – Price per Class A share

- 555,555,555 – Class A shares sold in the offering

- $75 billion – Total raised, the largest US IPO ever

- 42% / 79% – Musk’s equity stake / voting control

- 30% – Share of float allocated to retail investors

Why Forbes and Morningstar Disagree on the Price

Not everyone on Wall Street is buying what SpaceX is selling at $135. Morningstar’s equity research team put fair value at $63 a share, less than half the IPO price, and chief equity strategist Michael Field told clients to sit out the offering and wait for a more attractive entry point. The split between the IPO price and the most prominent independent valuation is now the central debate going into the first trading session.

The fundamentals are part of why. SpaceX is being sold at 92 times last year’s revenues, a multiple the FT called hefty. SpaceX’s 2025 consolidated revenue was $18.7 billion, the company posted a $4.94 billion GAAP net loss for the year, and adjusted EBITDA was $6.6 billion. The Starlink connectivity business is the financial engine, generating $11.4 billion in 2025 revenue at a 63% adjusted EBITDA margin, and the launch business turned in $4.1 billion. Investors paying $1.77 trillion are betting on Starship commercialization, on space-based AI data centers targeted for 2028, and on continued Starlink dominance, not on the 2025 numbers.

And yet the bid is real. The IPO was oversubscribed more than three times, with strong demand from both institutions and retail. Shadow markets implied a $2.3 to $2.4 trillion valuation before trading began. The Times Square protest is therefore pushing uphill: the demand is real, and the legal exposure SAIN is naming is also real. Both can be true on the same morning.

Who Actually Picks Up the Tab

The overlooked party in this IPO is the public shareholder, the one with no Class B votes, no seat on Musk’s board, and no ability to alter the S-1’s risk disclosures. SAIN’s 40-foot protest is a visual argument that the most consequential party in the deal is also the one with the least influence over it.

SAIN is not arguing against SpaceX as a business or against Musk as an entrepreneur. The coalition is arguing that public buyers, including retail investors entering through Robinhood, Fidelity, or Schwab, are being asked to absorb Grok’s legal, regulatory, and reputational liabilities for the price of one share of common stock at $135. The question SAIN’s installation puts to investors is not whether SpaceX will succeed, but whether the public shareholder is the one who should pay if the S-1’s flagged risks materialize in court.

SAIN’s installation stayed up through 7 p.m. ET on June 11. SpaceX shares begin trading on Nasdaq under the symbol SPCX on June 12, with Forbes calculating Musk could become the world’s first trillionaire the same day the S-1’s flagged risks first meet a public market price.

Frequently Asked Questions

What is Safe AI Now (SAIN)?

Safe AI Now is a coalition that describes itself as including faith leaders, child-safety organizations, family advocates, educators, technologists, and concerned citizens. The group entered the public conversation around the SpaceX IPO through its June 11, 2026 protest installation in Times Square. Its previous public activity has focused on online-safety advocacy, and it has no publicly listed leadership for the Times Square action.

Why is Grok the focus of the SpaceX IPO protest?

SpaceX completed its acquisition of xAI, the developer of the Grok AI chatbot, in February 2026 and folded Grok into a new AI segment. SpaceX’s own S-1 registration statement, filed May 20, 2026, flags Grok’s NSFW functionality as creating “heightened risks” and possible “reputational harm” tied to the generation of “nonconsensual or exploitative imagery.” SAIN argues that anyone buying SpaceX shares at the IPO price is buying into that exposure.

How much is SpaceX worth after the IPO?

SpaceX priced its IPO on the night of June 10-11, 2026, at $135.00 per share, raising $75 billion at a $1.77 trillion valuation, the largest IPO in US market history. The offering sold 555,555,555 Class A shares. Morningstar’s independent equity research put fair value at $63 per share, less than half the IPO price.

How much voting power does Elon Musk keep after the IPO?

Musk holds approximately 42% of SpaceX’s equity and approximately 79% of the voting control, the latter through super-voting Class B shares that carry 10 votes each. The S-1 discloses that SpaceX will be a “controlled company” under Nasdaq corporate governance rules following the offering, and that Musk will continue to control the outcome of matters requiring shareholder approval.

Geekbench 7 Launches and Erases Three Years of Scores

Google’s Selfie Video Sign-In Arrives as Deepfake Fraud Surges

Samsung’s New Galaxy Z Fold 8 Undercuts Its Own Ultra

Kroger and Brookshire’s Recall Over 19 Million Eggs for Salmonella

Mortgage Rates Hit an 11-Month High as Oil Fears Bite

Oil’s Price Shock Collides With Wall Street’s AI Spending Boom

Parsley and Cilantro Emerge as Cyclospora Suspects in North Carolina

Walmart Dresser Recall Reveals a Wider Furniture Safety Sweep

Apple’s iOS 27 Speed Fixes Echo Its 2018 Playbook

Cheshire Medical Center Cyclospora Cluster Exposes a Wider Outbreak

Pokémon GO Developer Niantic Rebrands as Scopely Explore

Persona 4 Revival Hands All Anime Cutscenes to Studio MAPPA

Doom Studio id Software Cuts Half Its Staff in Xbox Layoffs

Jaylen Brown Traded to 76ers for Paul George and Four Draft Picks

Nintendo Switch Online Adds Four Classics and One Japan-Only Title

Jordan Henderson Hospitalized After Wrist Injury at the Azteca

Meta’s Muse Image Lets Anyone Use Your Instagram Photos in AI

Mexico’s World Cup Run Ends at Azteca as England Hold On 3-2

Louis Vuitton Beats Molly Tea in China, Triggers Cultural Backlash

Pink Bearista Cup Returns July 13 as Starbucks Pink Vibes Drops

-

TECHNOLOGY3 years ago

TECHNOLOGY3 years agoHow to Adjust a Bulova Watch Band – An Easy Guide

-

News3 years ago

News3 years agoFred Pentland: Athletic Bilbao’s English mentor who changed the essence of Spanish football

-

FINANCE3 years ago

FINANCE3 years agoTax Planning for Every Season: Guide to Maximizing Your Tax Benefits

-

Education3 years ago

Education3 years agoAfrican Ministers New Education Plan

-

BUSINESS3 years ago

BUSINESS3 years agoWhat is Entrepreneurial Operating System? A Comprehensive Guide to EOS

-

Education3 years ago

Education3 years agoInnovate Your Learning Journey with Technology and Enhance Education

-

News3 years ago

News3 years agoRussians formally out of World Athletics Championships

-

BUSINESS3 years ago

BUSINESS3 years agoTop 9 Most Expensive American Cities to Rent an Apartment